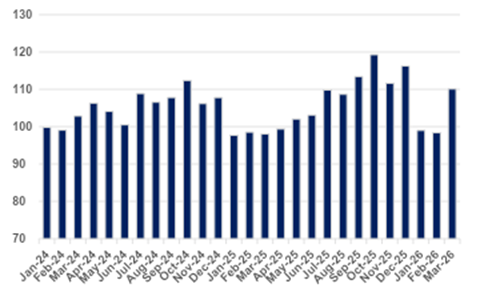

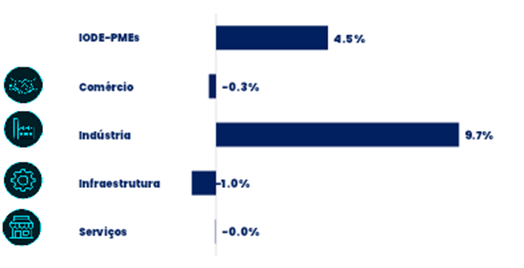

The Omie Index of Economic Performance of SMEs (IODE-PMEs) shows that the average real financial activity of Brazilian small and medium-sized enterprises registered growth of 4.5% in the first quarter of 2026, compared to the same period of the previous year. This marks the third consecutive quarterly increase in the index, overcoming the weak market performance in the first half of the previous year.

The IODE-PMEs acts as a thermometer of the economic activity of companies with annual revenue of up to R$ 50 million, monitoring approximately 750 economic activities distributed among the Commerce, Industry, Infrastructure, and Services sectors.

The relative improvement in the performance of SMEs in certain segments is based on some important pillars of the macroeconomic scenario. From a cost perspective, a significant relief for entrepreneurs has been observed in the recent period, especially in the first three months of 2026, when compared to the same period of the previous year. Based on the General Price Index – Market (IGP-M), calculated by FGV, we observe a relevant trend of cooling inflationary pressures: the accumulated rate over 12 months went from 8.58% at the end of the first quarter of 2025 to the current -1.83% at the end of the first three months of the year.

Despite the general trend observed in the index over the past year, it is important to highlight that the rise in fuel prices in March, resulting from the war in Iran, poses a new challenge to SMEs, especially due to short-term cost pressures across various production chains.

From a demand perspective, the resilience of the labor market — with unemployment still at historically low levels (5.8% in the quarter ending Feb/26) and real incomes significantly above those observed in the pre-pandemic period (+13% in Mar/26 compared to the 2019 average), in addition to a recent growth trajectory — contributes to sustaining household consumption.

On the other hand, consumer confidence contributed less to the positive performance of SMEs in the recent period. According to the FGV IBRE Consumer Survey, the confidence index showed an average decline of 1.1% per month between January and March 2026 in the seasonally adjusted series. Despite the increase in income, the fall in consumer confidence hinders consumption and investment decisions.

Restrictive credit conditions continue to hinder SMEs that are more sensitive to interest rates, maintaining pressure on the market in the medium term. At the most recent meeting of the Copom (Monetary Policy Committee) in March 2026, the committee reduced the Selic target rate by 0.25 percentage points to 14.75% per annum, initiating a cycle of interest rate cuts after a nine-month period with the rate at its highest level in the last two decades. The committee adopted a cautious tone due to geopolitical uncertainties in the Middle East, opening the possibility for a more contained rate reduction. Thus, despite the start of the cuts, it can be said that interest rates in the country remain at high levels and there is a risk of observing only a mild downward trajectory in the short term.

Maintaining high interest rates in the Brazilian economy for an extended period is already producing clear side effects on the business environment, reflected both in the slowdown of activity and in the sharp increase in default rates among individuals and businesses in the recent period. This context affects SMEs through two channels: on the demand side, by reducing consumption and access to credit; and on the costs side, by increasing the cost of working capital and raising default rates, putting pressure on margins.

From a sectoral perspective, the recent IODE-PMEs results once again highlight significant performance differences between segments, unlike what was observed in the second half of 2025. The industrial sector showed the most significant growth in the first quarter, with SMEs registering a 9.7% expansion in average real revenue compared to the same period of the previous year, maintaining its position as the main positive component of the index.

The recent strong performance of industrial SMEs was widespread across different segments of the manufacturing industry: of the 23 subsectors monitored, 19 showed positive results in the quarter, with particular emphasis on Machinery and Equipment Manufacturing, Paper and Paper Products Manufacturing, Wood Products Manufacturing, and Metallurgy.

SMEs in the service sector, in turn, had stable performance in the first quarter, interrupting the growth seen in the second half of 2025, in which they registered an average growth of 4.4%. Unlike the industrial sector, the IODE-Services index has shown, in recent months, a performance more concentrated in specific activities, with emphasis on Professional, scientific and technical activities (notably Architectural and engineering services), Human health and social services, and Transportation.

Nevertheless, it is important to highlight the continued weaker performance in segments relevant to the SME universe, with emphasis on Food and Education, which continue to face greater difficulty in recovering at the beginning of 2026.

In the Commerce sector, the index indicates that the average real revenue of SMEs ended the first quarter of 2026 with a slight decrease of -0.3% compared to the same period of the previous year, marking the fifth consecutive decline in the sector from a quarterly perspective. In the disaggregated analysis of the main segments, mixed results are observed: while wholesale remained positive and retail stable, the vehicle trade experienced a sharp decline.

Among the sectors with negative performance, SMEs in Infrastructure maintained their downward trend in the recent period, registering a 1.0% drop in the first quarter, after a 1.2% increase in the fourth quarter of 2025. As already pointed out in previous releases of the index, the negative result throughout the year reflects the slowdown in the construction supply chain, especially given the context of high interest rates in the country—a factor that discourages investment—impacting activities such as specialized construction services and building construction. Even so, the positive performance of the decontamination and waste management segment helped to prevent an even sharper contraction in the sector as a whole during the period.

Finally, the IODE-PMEs also allows for a regional analysis of the performance of Brazilian small and medium-sized enterprises. In the first quarter of 2026, the index reveals that the SME market remained in positive territory in the Southeast region (+3.8% YoY). The result is significant not only because it is the region that concentrates the majority of the country's active companies, but also because it reinforces the market recovery trend observed since Q3 2025.

The most recent regionalized data from IODE-PMEs also indicate continued growth in much of the country: in the South (+7.7% YoY), Northeast (+7.3%) and Midwest (+9.5% YoY). On the other hand, a slight contraction was observed, on average, in the North region (-0.6% YoY).

Projected growth of IODE-PMEs in 2026 revised to 2.2% following worsening inflation and Selic rate

Weaker performance in the SME market at the beginning of 2026, coupled with deteriorating short-term prospects for inflation and the Selic rate, led to a downward revision of the IODE-PMEs projection for the year. The estimate was revised from +2.9% to +2.2% compared to 2025 — a year in which the index registered modest growth of 1.2%. Even so, despite this revision and new challenges in the business environment, the scenario of moderate growth for SMEs in 2026 remains.

Despite a challenging economic context, marked by the maintenance of historically high interest rates and new external shocks, the main market players do not project an interruption in domestic economic activity. According to the median of expectations in the Central Bank's Focus Bulletin, GDP should grow by 1.9% in 2026, indicating a slowdown compared to previous years.

Amid a high degree of uncertainty, the resilience of household income and the labor market should sustain consumption in the short term—one of the main drivers for SMEs. While high default rates and volatile confidence put pressure on consumption, low unemployment and continued expansion of real income favor disposable income. In the first two months of 2026, real labor income was 5.3% higher than in the same period of 2025. In this context, the real adjustment of the minimum wage contributes to this movement, even if it amplifies fiscal challenges.

On the credit front, the scenario remains adverse for businesses. The expectation is for high interest rates to continue throughout the year. The intensification of tensions in the Middle East, with the war in Iran, has raised international oil prices and put pressure on global fuel inflation. In Brazil, the impact was quickly observed: the IPCA (Consumer Price Index) for March 2026 registered significant increases in diesel (+13.9%) and gasoline (+4.59%) prices. This movement is worrying because, in addition to compromising family income, it increases the cost of important production chains, such as food.

In this context, inflation expectations have been revised upwards, recently reaching 4.8%, above the upper limit of the target for the year. In response, projections for the Selic rate have also increased, with expectations of 13% by the end of 2026 — above the 12.25% projected at the beginning of the year.

In summary, the more adverse global inflationary environment imposes additional challenges on SMEs in the short term, with higher cost pressures, slower demand growth, and expensive and restricted credit. The Omie Survey of April 2026 reflects this scenario: entrepreneurs demonstrate a predominantly cautious outlook, projecting stability or only marginal growth for their businesses.

Given this, 2026 demands greater prudence from entrepreneurs, in an environment marked by high uncertainty and macroeconomic volatility, both domestically and internationally. Added to this is the electoral calendar in the second half of the year, which tends to reinforce a more conservative stance in investment decisions. More than just following election polls, it will be crucial for business owners to understand the challenges facing the next government, especially in the fiscal area.

Finally, in addition to the challenging macroeconomic scenario, entrepreneurs are also beginning to grapple with the biggest structural transformation of the Brazilian economy in decades: the Tax Reform. Although its effects in 2026 are still limited—especially for micro and small businesses—the moment demands preparation and understanding of future changes. The Omie Survey reveals a worrying fact: about half of SMEs have not yet started or are in a very early stage of preparing for the Reform. With the advancement of the transition and the approach of relevant milestones, the time for planning is reduced, increasing the risk of loss of competitiveness for a significant portion of the market.